In terms of financial matters, women have come a long way over the last few decades. From the days when a man was a plan, and the ‘fairer sex’ relied on their fathers or husbands for security, women have only become more independent and financially savvy. That’s not to say there is no room for improvement, you just have to look to the gap in relation to wage parity to know that we still have a way to go. Although the gender pay gap in Australia is decreasing over time to a new current low of 16%, women tend to dominate in lower paid industries and be under represented in senior roles and on boards.

That said, this is changing, stats published on International Women’s Day this year show that there are more women on ASX top 20 boards than ever before – now over 30 per cent. The proportion of female enrolments in traditionally male-dominated courses, like information technology, has grown by nearly 12% per year for the past five years. Encouragingly, the number of women working in the best paid industry (mining) has quadrupled over the past 20 years. While it is heartening to see these changes, the fact remains that Australian women are still struggling to save enough for retirement.

Closing the final gaps

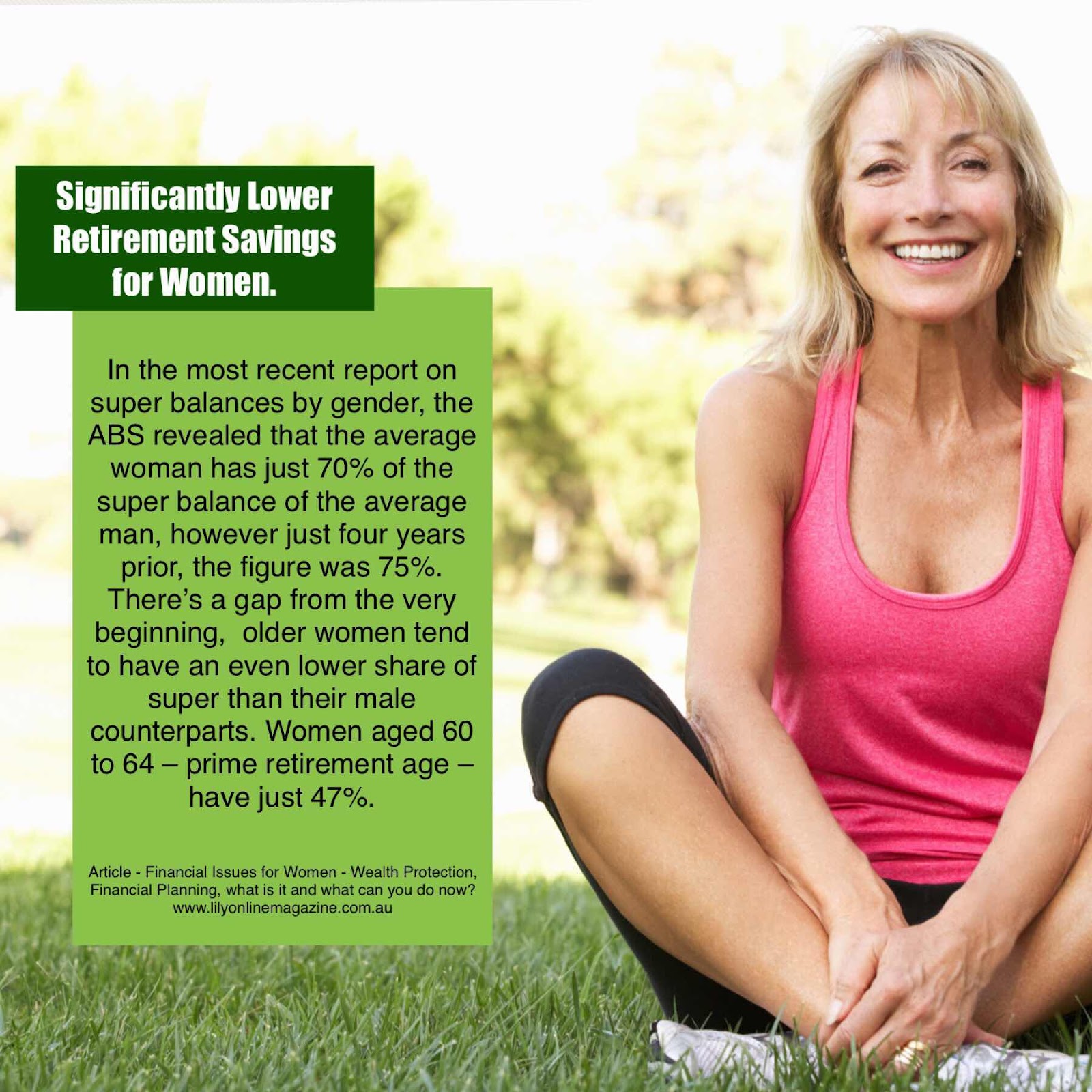

In the most recent report on super balances by gender, the ABS revealed that the average woman has just 70% of the super balance of the average man, however just four years prior, the figure was 75%. There’s a gap from the very beginning, older women tend to have an even lower share of super than their male counterparts. Women aged 60 to 64 – prime retirement age – have just 47%.

There are a few different theories as to why this is. The first and most obvious is that many women take a significant amount of time off work to have children. Nearly 20% of women permanently leave their jobs before the birth of their children, meaning they have to re-enter the workforce afresh after a significant career break. Around 16% of women take just one to four weeks’ paid leave, with the rest of their leave being unpaid. Many couples don’t even think about the fact that super isn’t generally paid on parental leave payments. Even if a woman has parental leave and only takes the maximum 18 weeks’ leave, that’s still a significant loss of earnings.

Another theory suggests that risk appetite is also having an impact on women’s super balances, compounding the impact of time out of the paid workforce. Women may be psychologically predisposed to be conservative with their superannuation investment choices. One survey found that only 30% of women have a ‘high risk’ allocation in their super, 7.5% lower than men. In other words, taking the time to examine your biases against risk could pay off.

It is important to seek professional help with your financial journey when it comes to superannuation, investments and insurances. There is a lot you can do to take back the power and change your financial future. So what things can you do right now. Research has put the share of the population living pay day to pay day at between 32 per cent and 46 per cent. What’s more, many Australians say they don’t have (or couldn’t raise) even $500 to pay for an unexpected expense. In a way, these numbers reflect the laidback ‘she’ll be right’ attitude that pervades our culture. But the reality is that we all live with risks, both big and small, that we can’t avoid.

That’s where a financial safety net comes in handy. Making sure that you are prepared for financial setbacks or unanticipated costs does not come down to any single measure. Rather, it’s a comprehensive approach to risk that’s designed to protect you and your family’s financial wellbeing, come what may.

Maintain a rainy day fund

The first line of financial defence for women is to have some money tucked away in a ‘rainy day’ fund for emergencies and unexpected costs. If you are living from one pay day to the next and your hot water heater bursts or your car needs urgent repairs, the temptation is to whip out the credit card. If you are only able to make the minimum monthly repayment you could be paying off that hot water heater for years to come. Whereas paying cash will save you money and make your financial goals that much easier to achieve.

Most experts suggest you aim to put aside three to six months’ living expenses. This can take a while to build up so one time-honoured strategy is to ‘pay yourself first’. It’s a good idea to keep your emergency cash in a separate account from your everyday money.

Reduce debt

Even with the best willpower in the world it can be difficult to save if you are weighed down with debt. The good news is that with interest rates at or near their historic lows, there is no better time than the present to tackle debt. Aim to pay down loans with the highest interest rate first – typically this will be your credit cards. If you have a mortgage, aim to pay more than the minimum monthly payment. By keeping at least three months ahead of schedule you can build a buffer to provide some wriggle room with your lender if you experience financial difficulties.

Review insurance

No financial safety net is complete without adequate personal insurance. We tend to insure our car and our house before we think about our most precious possession, our health and our ability to earn an income. While health insurance will cover some of your medical costs, it won’t pay the mortgage and food bills or take care of your family while you are unable to work. Worse still, what would happen if you were to die prematurely? That’s where personal insurance comes in, to cover your life, total and permanent disability, trauma and income protection. It’s possible you already have cover for some of these through your superannuation fund, but it may not be sufficient. It’s important to make sure you know where you stand on these. Seek professional help if needed and conduct a review of your situation. Then work towards having a plan that you and your family are comfortable with.

Follow us for more articles to come.

Written by Sam Tabit

Senior Financial Planner

Bamboo Wealth

www.bamboowealth.com.au